How to Keep Irregular Expenses From Disrupting Your Cash Flow

Photo by Alexander Grey on Unsplash

Most of us have a handle on our fixed expenses:

- Mortgage/rent

- Car payment

- Netflix subscription

You are also probably familiar with your flex expenses that happen as a part of daily living:

- Food

- Gas for your car

- Date nights, etc.

But in my experience most often what tends to derail someone’s savings strategy, or what could unexpectedly drain the cash reserve, are the mysterious “irregular expenses”.

These expenses, also known as “Non-monthly recurring expenses” are the big expenses that tend to pop up at irregular intervals and can short-circuit your monthly budget. They might come due once a year, every six months, every quarter, or seemingly at random. These expenses can include things we choose to spend money on such as:

- Travel

- Charitable Giving

- Gifts and Celebrations

and not so fun categories like:

- Certain taxes

- Insurance premiums

- Home maintenance.

Dealing with these large and oddly timed expenses can be a challenge. A workshop hosted by budget guru Natalie Taylor at the annual XY Planning Network conference in 2023 shines some light on how to deal with these cash flow speed bumps more effectively.

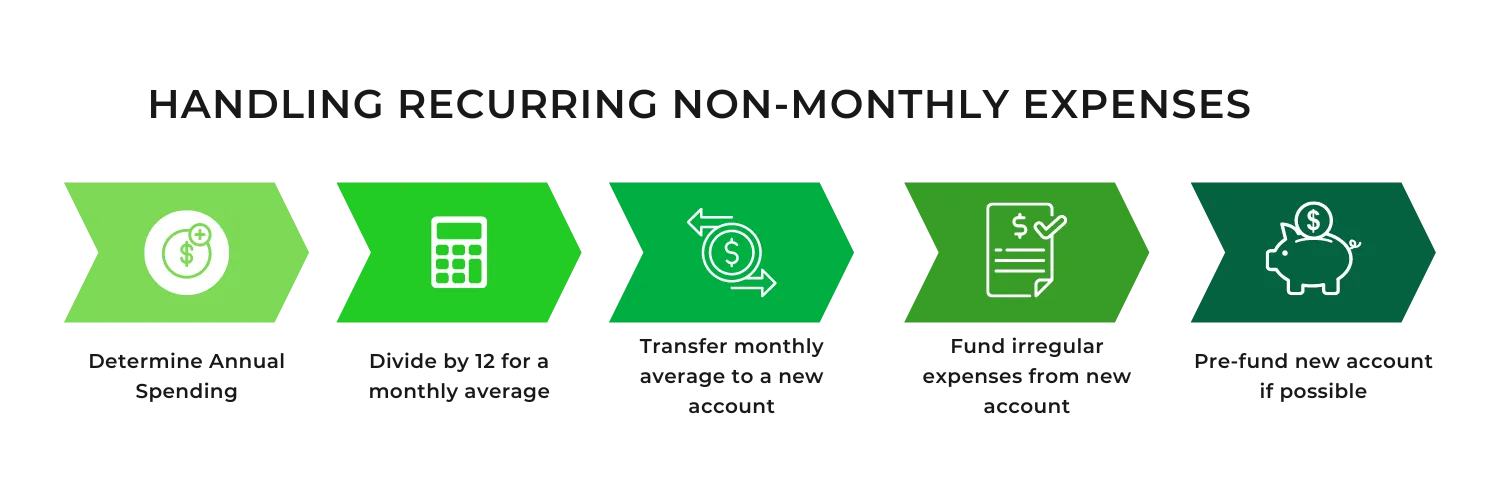

- Determine your annual spend on non-monthly recurring expenses.

- Many of these expenses are known in advance such as an annual or semi-annual insurance premium or an annual property tax bill.

- Others should be estimated or budgeted such as travel and home maintenance. Recent history of spending in these categories can be helpful, and Monarch Money is an app I use with clients to track and categorize spending over time.

- Divide by 12 to come up with an average monthly spend on these expenses.

- This converts this category from a number that surprises you and derails your budget to a monthly number you can account for in your regular spending.

- Set up a monthly transfer of the average monthly spending on irregular expenses (determined in step 2) to a separate savings account.

- Now these expenses are a true part of your monthly spending, and you can plan your other spending around them accordingly.

- Use the money from this new savings account to pay these irregular expenses as they occur.

- When that insurance bill comes due, or when you book your next cruise, pull from the money you have been setting aside for this very purpose.

- Not only will your budget and your emergency reserves stay intact, you won’t have to reach for the credit card for that new refrigerator.

- If possible – seed the new savings account with 3 – 6 months of average non-monthly expenses.

- While this may not be possible for everyone, ideally you want to give yourself a little head start, as a particularly expensive month with a couple of large items could use more cash than you’ve been able to put away just yet.

By taking these one time “surprise” expenses and making them a part of your monthly budget, you can stay on top of them and always have cash on hand. Instead of having to say “December was a tough month, but we’ll get back on track once we pay these expenses down,” you can reach for the money already identified for those expenses, and carry on with less stress and without interrupting your plan.

So give this framework a try for handling irregularly timed expenses, let me know how it works for you, and if you think you need more support schedule a call to learn more about how we can work together.

You may also like

Teaching Your Young Children About Money