Getting Comfortable with Market Volatility

Photo by Anne Nygård on Unsplash

Losing money, even temporarily, even just “on paper,” is a very uncomfortable thing. Loss aversion leads us as humans to weigh and remember losses much more heavily than gains of the same amount. That happens even if the gains are greater, and happen more frequently than losses, which is common with the stock market.

But if we are going to grow our money to outpace inflation and provide for future goals such as retirement, college tuition for our kids, or buying that vacation home, we need to get comfortable with short term market volatility. Otherwise, panicking in the short term can cause us to miss great opportunities in the long term. Keep the following points in mind.

- Market downturns happen way more often than you think.

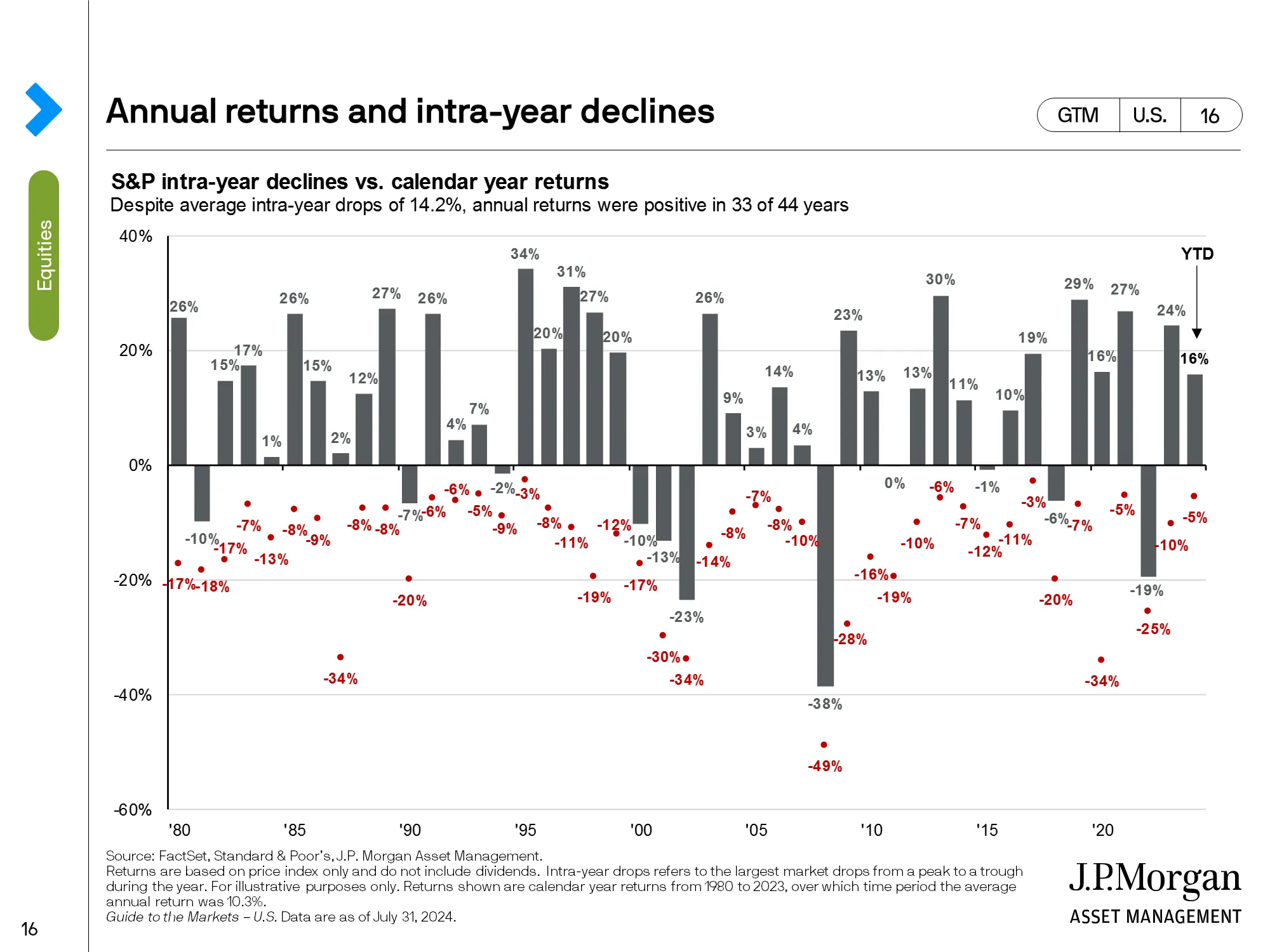

- From 2000 to 2023 the S&P 500 (the index of the 500 largest publicly traded companies in the United States), has had a drop of at least 10% in 16 of those 24 years.

- We often forget about this, because despite those downturns, the index finished up for the year in 8 of those 16 years with drawdowns of at least 10% (and one additional year the market finished just about even before dividends).

- Moral of the story: Short term downturns, even when they are 10% or more, are often reversed within the current year.

- Despite routine and sometimes scary market drops, the S&P 500 has historically been up for the year much more often than it has been down.

- Since 1928 the S&P 500 has finished up for the calendar year 67 times vs down 30 times. That’s a little more than two thirds of the time, or about 69%. Source.

- Consecutive years of underperformance are even more rare, happening only 8 times over the 1928 – 2023 stretch.

- Moral of the story: Avoiding the stock market because of concerns over a downturn, when you have a long enough time horizon*, means you are going against historically favorable market odds. See the end of this blog for an important note on time horizon.

- Quick market swings mean you can miss out on the recovery if you sell after a drop.

- August 2024 is a great example of this. In three trading sessions from August 1st – August 5th the S&P500 was down over 6%. It would have been easy to start to feel a sense of panic.

- However, by mid-day August 15th the index was back to where it started the month. Roughly 8 trading days to recover.

- February – August 2020 and the 2022 – 2023 time period are two other recent examples of fairly quick declines and recoveries.

- Moral of the story: Markets can move quickly, and trying to time the market means you have to be right twice – when to buy and when to sell. Once the market has already moved down, selling makes the paper loss a real loss. Sometimes the market recovers before you can convince yourself it’s ok to re-invest. Instead, make sure you are invested properly before the next market downturn and stay the course, or better yet view market dips as a possible opportunity to invest more funds.

*One final point on time – how long you have to go before you need the money is important because time is what allows you to ride out market corrections.

- Short-term money should be in cash or other secure investments.

- Money you’ll need in a few years, but not right away, should be invested somewhat conservatively to protect from market downturns.

- Money you won’t likely be accessing for 5 or more years can be invested in more aggressive portfolios, subject to the ups and downs of the market in the meantime.

- Remember – even if you’re retired and taking money out of your investment portfolio – you should never need all of the money at once. Even a retirement portfolio can have a mix of ultra safe short-term assets, more conservative investments for the coming years, and more aggressive investments to help keep up with inflation all in the same portfolio.

So remember that market volatility is a part of investing and it probably happens more than you realize. If you're watching your accounts closely, in the moment the downturn can seem like "the big one" and panic can set in if you're not prepared. But as we have seen with other downturns the recovery eventually comes, and today's market volatility quickly becomes a distant memory.